Categories

18 Apr, 2026

Savvy News

Buy now, pay later services have made significant inroads with Canadian shoppers since 2020. Afterpay, Klarna, Sezzle, and Affirm now appear at checkout on thousands of Canadian retail sites and some in-store terminals. The pitch is simple: split your purchase into four equal payments, usually every two weeks, with no interest.

$8

Afterpay late fee per missed payment

3–6%

merchant fee for accepting BNPL

0%

credit score improvement from BNPL (no positive reporting)

30%

max APR on some Affirm longer-term plans

That sounds better than a credit card. Whether it actually is depends on what you compare and what happens when something goes wrong.

How BNPL works in Canada

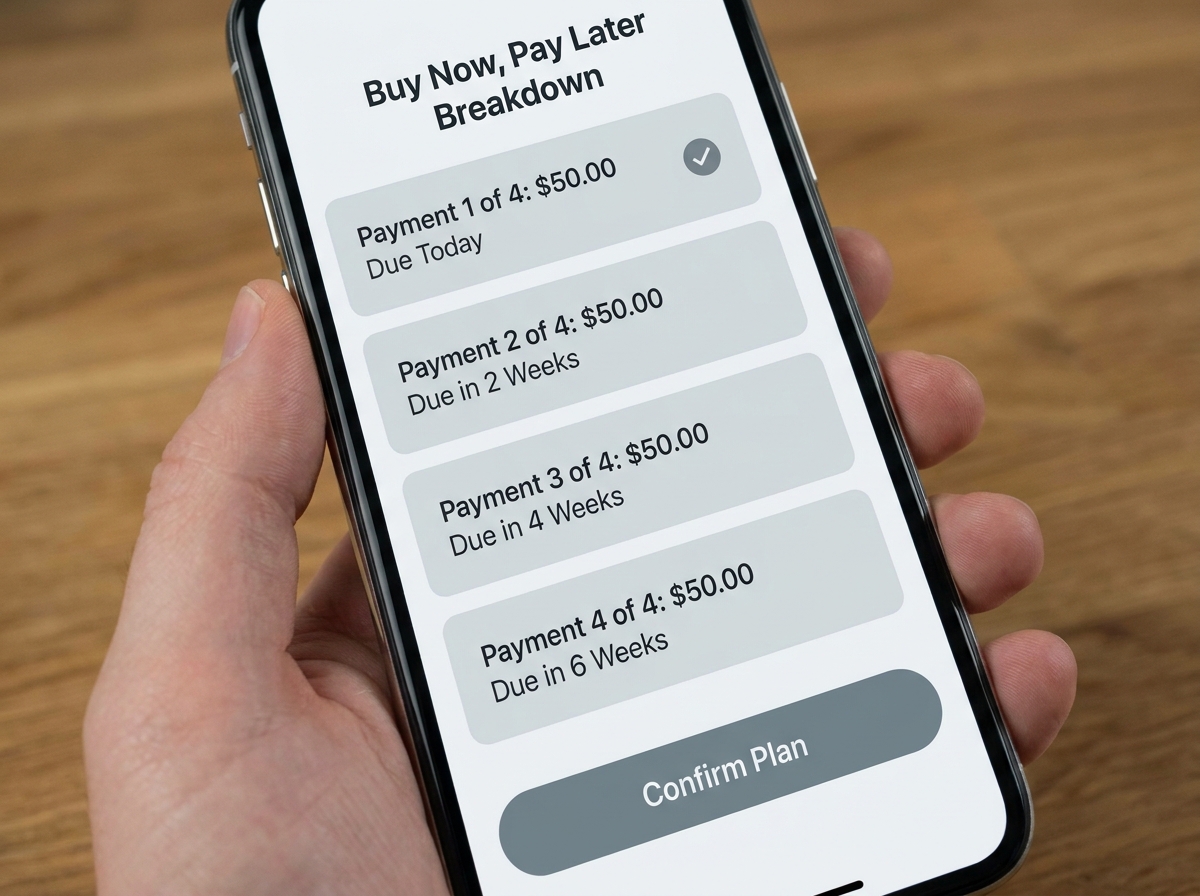

The standard BNPL model splits a purchase into four equal bi-weekly payments. A $200 jacket becomes four payments of $50, two weeks apart. If you make all payments on time, you pay $200. No interest. The merchant pays the BNPL provider a processing fee (typically 3% to 6% of the transaction), which is why retailers offer it despite the cost.

Late fees apply when payments are missed. Afterpay charges $8 per missed payment, capped at 25% of the order value. Klarna varies by plan. Affirm offers longer-term installment loans at 0% to 30% APR depending on the merchant and your credit profile. The "pay in four" model is interest-free. The "pay over 12 months" model often is not.

What BNPL does not give you

This is where the comparison to credit cards becomes significant.

No rewards. BNPL transactions do not earn credit card points, cashback, or miles. If you were going to pay with a 2% cashback card, using BNPL costs you that 2%. On a $500 purchase, that is $10 in foregone rewards.

Limited consumer protections. Credit card chargebacks are a powerful consumer protection tool. If a merchant fails to deliver a product or delivers something materially different from what was sold, you can dispute the charge with your card issuer and typically get your money back. BNPL dispute processes are handled by the BNPL provider and are generally less robust than card network dispute mechanisms.

No credit building. Most BNPL providers do not report on-time payments to Canadian credit bureaus. Some report missed payments. This means BNPL is a one-way credit instrument: you can hurt your credit score with it but not improve it.

No purchase protection or extended warranty. If you bought on a credit card with purchase protection, that coverage applies. BNPL has no equivalent.

Where BNPL genuinely makes sense

The honest answer is that BNPL makes sense in specific circumstances that do not apply to most credit card holders.

- You do not have a credit card and need to split a large purchase. If you have no access to credit otherwise, interest-free BNPL is dramatically cheaper than a payday loan or a high-interest personal loan.

- You have a card but know you will carry the balance. If a $600 purchase would sit on your card at 19.99% for four months, BNPL at 0% saves you roughly $40. The math works if you will definitely make the BNPL payments on time.

- The merchant has a direct discount for BNPL users. Some retailers offer a promotional discount on BNPL purchases. If the discount exceeds the value of credit card rewards you would have earned, BNPL wins.

The hidden cost: spending more than you planned

Research on BNPL consistently shows that splitting payments increases average transaction sizes. When a $400 camera becomes four payments of $100, it feels more affordable than $400 upfront. This is a feature, not a bug, from the retailer's perspective. For the consumer, it can mean spending more than originally intended.

Credit cards carry the same psychological risk. But the credit card statement at the end of the month shows you one consolidated number. BNPL spreads multiple small amounts across multiple services on different timelines, making it genuinely harder to track what you owe in total.

BNPL vs Credit Card Cost Calculator

Compare the true cost of Buy Now Pay Later vs. paying with a cashback credit card.

The regulatory environment in Canada

BNPL in Canada is relatively lightly regulated compared to credit cards. Credit card issuers are subject to the federal Bank Act, disclosure requirements, and the Financial Consumer Agency of Canada's oversight. BNPL providers operate with fewer consumer protection requirements, though the Financial Consumer Agency has been reviewing the space and regulation is expected to tighten.

For now, if you use BNPL, the practical protections are weaker than what you get with a major credit card from a Canadian bank.

Frequently asked questions

Does using buy now, pay later hurt my credit score?

Most major BNPL providers do a soft credit check or no credit check at approval, which does not affect your score. Late or missed payments are where it can hurt. Some providers have started reporting to credit bureaus, but this is not yet standard across all BNPL services in Canada. Check the specific provider's policy.

Can I use a credit card to pay off a BNPL balance?

Usually not. BNPL providers typically debit your bank account directly or allow debit card payments. Paying off BNPL with a credit card is often not permitted. This also means you cannot earn credit card rewards on BNPL transactions even indirectly.

Is Affirm the same as Afterpay and Klarna?

They are similar but not identical. Afterpay and Klarna's primary product in Canada is pay-in-four with no interest. Affirm offers a wider range of plans, including longer-term financing at interest rates that can reach 30% depending on the merchant agreement and your credit profile. Read the terms carefully for Affirm plans that extend beyond the standard pay-in-four window.

For most Canadians who pay their credit card in full, a rewards credit card beats BNPL on every metric that matters: consumer protection, rewards, credit building, and ease of tracking. BNPL has a role, but it is a narrower one than the marketing suggests.